— For Self-Employed Workers &

Sole Proprietors

Filed within 48 hours and receive your Refund Check within 8-12 weeks! Currently it's within 9 weeks!

No Upfront Fees

Pay After you receive your checks

SETC is calculated with eligible days and your income.

Current SETC average per Client is $4,688.89 or more.

Tax Credits Claimed

$0B

Years in Business

0 Years

Successfully approvedINSUREDGUARANTEED REFUND POLICY

0%

First Come, First Serve!

Pay After you get

your checks

PAY AFTER You Get your SETC Checks

Absolutely NO RISK

Pay US when you get Paid

Pay Upfront

(discounted rate)

Still No Risk: 100% Guaranteed in writing

Pay After Calculations are done

Pay Plans Available

(PayPal Pay Later)

Both Pay After & Pay Upfront

Options Include:

E&O Insurance Coverage

Audit Defense Protection

SETC Comprehensive Report & Mailing Your Application

100% SuccessRate

100% money-back Guarantee

Its all stated in your

agreement!

Affordable Payment plans forUpfront Fee Option (6, 12, & 24 Months)

Pay After you get

your checks

PAY AFTER You Get your SETC Checks

Absolutely NO RISK

Pay US when you get Paid

Pay Upfront

(discounted rate)

Still No Risk: 100% Guaranteed in writing

Pay After Calculations are done

Pay Plans Available

(PayPal Pay Later)

Both Pay After & Pay Upfront

Options Include:

E&O Insurance Coverage

Audit Defense Protection

SETC Comprehensive Report & Mailing Your Application

100% SuccessRate

100% money-back Guarantee

Its all stated in your

agreement!

Affordable Payment plans forUpfront Fee Option (6, 12, & 24 Months)

about us

Compassionately Compliant in Tax, Accounting, & Legal

Top Rated Tax Firm since 2017

100% Successfully Approved

Upfront or Installments, YOU Decide!

It's not a loan & it's tax free!

We know IRS Tax Credit Codes which they DO NOT know!

Compassionately Compliant in Tax, Accounting, & Legal

Upfront or Installments, YOU Decide!

It's not a loan & it's tax free!

We know IRS Tax Credit Codes which they DO NOT know!

our features

You will never have to pay for a mistake WE make, GUARANTEED! Our SETC work is 100% insured AND we give it to you in writing!

Data security

Audit protection in writing

Licensed tax professionals

100% Guaranteed

Team Expert

April 15th, 2025

we know tax credits

Hospitality

$3M+

Retail

$3.6M

Education

$187K

Transportation

$942K

Construction

$3.01M

Education

$201K

Hospitality

$5M+

Retail

$1.92M

Transportation

$1.21M

Transportation

$731K

Restaurant

$897K

Hospitality

$3M+

Construction

$133K

Education

$738K

Restaurant

$581K

Manufacturer

$2.82M

Healthcare

$3.6M

Healthcare

$578K

Healthcare

$1.07M

Farming

$926K

Retail

$2.82M

Hospitality

$3M+

Retail

$3.6M

Education

$187K

Transportation

$942K

Construction

$3.01M

Education

$201K

Hospitality

$5M+

Retail

$1.92M

Transportation

$1.21M

Transportation

$731K

Restaurant

$897K

Hospitality

$3M+

Construction

$133K

Education

$738K

Restaurant

$581K

Manufacturer

$2.82M

Healthcare

$3.6M

Healthcare

$578K

Healthcare

$1.07M

Farming

$926K

Retail

$2.82M

Education

$1.9M

Restaurant

$1.55M

Service

$927K

Staffing

$1.15M

Construction

$187K

Construction

$1.31M

Healthcare

$7M+

Education

$3.6M

Construction

$187K

Construction

$1.05M

Construction

$521K

Hospitality

$5M+

Hospitality

$7M+

Hospitality

$10M+

Engineering

$2.22M

Construction

$3.49M

Restaurant

$4.66M

Non-profit

$1.34M

Hospitality

$5M+

Hospitality

$10M+

Education

$1.9M

Restaurant

$1.55M

Service

$927K

Staffing

$1.15M

Construction

$187K

Construction

$1.31M

Healthcare

$7M+

Education

$3.6M

Construction

$187K

Construction

$1.05M

Construction

$521K

Hospitality

$5M+

Hospitality

$7M+

Hospitality

$10M+

Engineering

$2.22M

Construction

$3.49M

Restaurant

$4.66M

Non-profit

$1.34M

Hospitality

$5M+

Hospitality

$10M+

don’t lose your chance!

![]()

testimonials

about setc

The Evolution of SETC (qualified sick and family leave credits) The Families First Coranavirus Response Act (FFCRA) is a Federal Law (Public Law No. 116-127) and as amended and extended by the Tax Relief Act of 2020 (the Tax Relief Act).

View IRS Tax Code

IRS approved

e-file tax provider

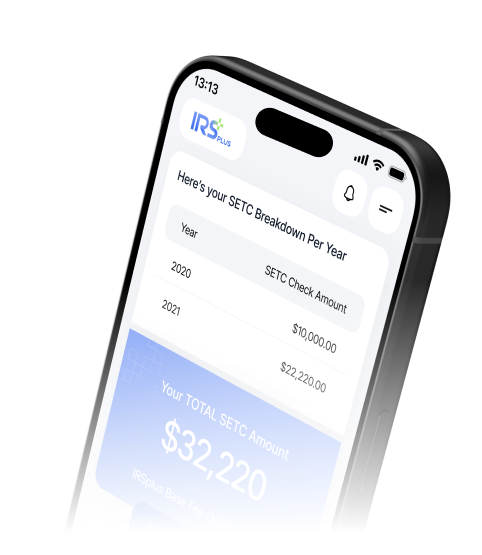

Coronavirus Paid Leave Tax Credit for Self Employed Workers paying up to $32,220

NOT a loan-refund of taxes you already paid. Not taxable

FFCRA helps Independent business owners and contractors receive money for not being able to work during Covid

FFCRA Act to include self-employed persons for the first time (Sections 7002(a) and 7004(a) of Public Law No. 116-127).

$50B approved for SETC — It’s first come first serve

Your money that is set aside from the Government. Take it or leave it! Up to you!

No COVID test required. You qualify if you have self employed earnings during 2020 & 2021 and work as:

Audit Protection

100% Guaranteed

Did you miss work due to:

— Federal, state, or local lockdown orders related to COVID-19

— Quarantining or isolation order related to COVID-19

— Caring for your child whose school had closed or gone virtual (Remote Learning)

— Caring for your child because your child care provider was unavailable due to COVID-19

— Symptoms of COVID-19 or seeking a medical diagnosis

— Sickness due to vaccination side effects

— Caring for someone with COVID symptoms

— A COVID-19 vaccination appointment

— Side effects due to vaccination

assurance

Our tax and government order specialists ensure the accuracy of your SETC

our work backed by insurance

Many CPAs outsource these types of applications because they too know that its not under their umbrella of comfort.

![]()

Professional Liability Errors & Omissions Insurance

we are tax professionals

We also love doing what's in our best interest and choose Tax Professionals according to what we are filing for. The IRS Tax Code is over 70,000 pages and we don’t expect our CPA to waste time trying to learn that for a limited time tax credit! We have all the Covid-19 government orders and invested heavily ($$$) to acquire them because this is OUR field of expertise.

![]()

100% Successfully Approved

we are trusted

If you really love your CPA, don’t expect them to educate themselves on government incentives too. Let them use their time and energy on saving you tax dollars properly.

![]()

Data security & customer care

100% guaranteed

We do everything in house and have a tight handle on the entire process. Your CPA cannot give you this!

![]()

Qualification underwriting report

scroll down

don’t lose your chance!

The most important thing you'll do in 2024 is meet this deadline!

1099 Contractor

Single Member LLC

Married with kids

$64,440 refund

Filed Schedule C or SE

Self Employed

Sole Proprietor

We are licensed tax professionals and we are IRS compliant.

Yes! I choose a Tax Credit Specialist to file for me!Get Started Now!It’s first come, first serve! Don’t miss out!

Yes! I want to file by SETC with a Tax ProAbsolutely! This particular tax credit refund is designed with self-employed individuals in mind. It's also a great fit for small business owners, freelancers, and anyone working as a 1099 contractor. It's all about giving a helping hand to those who run their own show in the business world.

Yes, you can! If you've got self-employment income alongside your W2 earnings in 2020 or 2021, you're in the running for SETC tax credits. Just remember, if you received FFCRA wages through your employer, we'll need to adjust your SETC credit accordingly to avoid double benefits. And if your employee benefits don't cover everything, you might still be able to claim extra credits based on your self-employment.

No, it's not. Here's the good news: unlike Paycheck Protection Program (PPP) and the Employee Retention Tax Credit (ERTC), the Self-Employed Tax Credit (SETC) is not considered taxable income. This means when you claim SETC, it doesn't add to your tax burden the way PPP and ERTC might have. It's a financial perk without the extra tax strings attached.

Actually, no. Filing for the SETC tax credit won't affect your 2023 income tax filings at all. To access these credits, our in-house team of accountants will amend your previously filed taxes for 2020 and/or 2021. This means the process is retroactive and doesn't touch your 2023 tax situation. It's a separate adjustment to your past filings, ensuring that your 2023 taxes remain unaffected.

Absolutely! If both spouses have self-employed income and individually qualify, they can each receive the maximum SETC of $32,220. However, it's important to note that they cannot share qualifying COVID days for children. Each spouse must meet the eligibility criteria based on their own separate self-employed activities and COVID-impacted days. This allows both individuals to fully benefit from the credit, provided their individual circumstances align with the SETC requirements.

The size of your SETC tax credit hinges on a few key elements:

These elements collectively contribute to determining the tax credit you can expect. For a precise calculation, you might want to use a specialized tax credit calculator or consult a tax expert.

The Client fee is a percentage of your total SETC refund. Our team of tax professionals will qualify, calculate and prepare all required paperwork ensuring your SETC application is filed within IRS compliance. We consider all tax codes and tax laws required to do this properly.

Fees are due once your application is complete and ready to file. Fees can be paid all at once or you can opt to pay in installments through PayPal.

For fees equaling $1,500 or less, choose to pay over 6 months interest free or in (4) interest free installments starting at the time of filing, with (3) subsequent repayments every 15 days.

For larger refunds with Client fees greater than $1,500, you can finance your payments monthly with PayPal Pay Later. The “Pay Monthly” installment application is quick and simple.

With this option you may select to pay over the course of 6, 12, or 24 months. You must also have a PayPal account in good standing or open a PayPal account to apply. If you do not see monthly option available on your account, please contact PayPal directly.

Please note: It is not required to have a PayPal account to make a payment upfront, you can use your debit card or credit card at checkout.

Our Guarantee: If you do not receive your tax credit for any reason, we will reimburse you any fees paid.

Paying with PayPal pay later is quick and simple. It offers an affordable option for clients to pay over 2, 6, 12, or 24 months. Even though Clients generally receive their SETC checks in less than 4 months, they are not required to pay off their PayPal installments.

Many clients opt to choose a 24 month pay later plan. An invoice of $2,000 on this plan would have an estimated monthly payment of $85. SETC checks arrive within 4 months so the estimated monthly payments amount would total $340 before checks arrive.

To pay your Client fee without logging into a PayPal account, you may simply select the “debit or credit card” button in the Client portal invoice page.

While SETC (Self-Employed Tax Credit) and FFCRA (Families First Coronavirus Response Act) are both born from the same legislative umbrella aimed at providing COVID-19 relief, there's a neat distinction in their applicability:

So, while they share a common goal of easing the COVID-19 burden, SETC and FFCRA divvy up their support based on your employment status SETC for the self-starters and FFCRA for the employed brigade

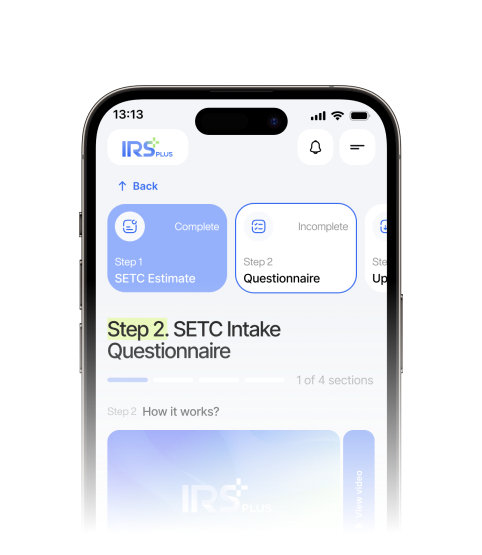

Not at all. It's really straightforward – just select your days in our questionnaire. Then, upload your 2019 to 2021 tax returns and a copy of your driver’s license, and sign our agreement. That's it! We handle the rest, ensuring a smooth and stress-free process for you.

The FFCRA (Families First Coronavirus Response Act) is a federal response to COVID-19, originally passed in March 2020. It started by aiding employers with W-2 employees, offering paid sick leave and unemployment benefits. By December 2020, under the CARES Act, it expanded to include the self-employed, freelancers, and gig workers, providing them with tax credits for lost work due to COVID-19. This broadened its scope, making it a comprehensive support system during the pandemic.

The FFCRA tax credit can reach up to a substantial $32,220.00, with its calculation rooted in your self-employed net earnings for both 2020 and 2021.

It's not uncommon to be in the dark about the FFCRA tax credits. Initially, the focus of the FFCRA was on employers with W-2 employees. When the CARES Act came into play later in the same year, expanding these tax credits to include the self-employed, it didn't get the spotlight it deserved.

This lack of widespread publicity is a key reason why many self-employed individuals remain unaware of their entitlement to these credits. In fact, research indicates that over 80% of self-employed persons are still in the dark about their eligibility for the FFCRA tax credits.

Staying abreast of such updates is crucial, especially when they can have a significant financial impact.

The PPP (Paycheck Protection Program) and the FFCRA (Families First Coronavirus Response Act) are indeed both responses to the economic fallout of COVID-19, but they cater to different needs.

PPP's Role: The PPP is all about bolstering small businesses. It does this by offering loans, which can be forgiven if used primarily for payroll and other eligible expenses. It's essentially a financial lifeline for businesses to keep their teams employed during the pandemic's challenging times.

FFCRA's Focus: On the other hand, FFCRA is not about loans but about providing tax credits. These credits are applied to taxes that individuals, especially the self-employed and employers, have already paid. Unlike the PPP, which is designed to support businesses directly, FFCRA is more individual-focused, offering relief to people impacted by COVID-19 related work disruptions.

While both play crucial roles in pandemic relief, their mechanisms of support differ significantly - one through loans for businesses and the other through tax credits for individuals

When determining eligibility for the SETC (Self-Employed Tax Credit), it's your net self-employed income that's under the microscope. This means you need to have a positive net income, which is your earnings after all allowable business deductions, for either 2019, 2020, or 2021. Additionally, your eligibility hinges on having specific days that qualify under the COVID-related criteria. It's this combination of positive net income and qualifying days that shapes your eligibility for the SETC.

The amount of the tax credit you can receive is determined through a combination of specific criteria:

Income and Days Affected by COVID-19: Your average daily self-employment income and the number of days you missed work due to COVID-related issues, like quarantine or symptoms, are pivotal. This is used to calculate your potential credit.

Child Care Credit Calculation: If you took leave for childcare, your credit is the lesser of your average daily self-employment income or $511 per day.

Self-Employment Work Interruption Credit: If you missed work due to personal COVID-19 issues or caregiving, the credit is the lesser of two-thirds of your daily income or $200 per day.

Net Income and Caregiving Factors: Your net income reported on Schedule C for the tax years 2019-2021, the days you were sick or quarantined, and the time spent caregiving due to COVID-19, including periods when schools or daycare were closed, all play a role in the calculation.

Our Client Portal simplifies this process, guiding you through these factors and helping calculate your maximum FFCRA tax credit. For a quick estimate, our online Tax Credit Calculator can provide an accurate assessment of your eligibility and the likely credit amount.

The average FFCRA refund received by IRSPlus customers typically stands at around $15,000. This figure, specific to IRSPlus's clientele, offers insight into the substantial relief that the FFCRA program has provided to individuals affected by the pandemic. It's important to note that this amount can vary based on individual circumstances, but for IRSPlus customers, $15,000 is the average benchmark.

Get ready for a nice surprise in your mailbox! The IRS will dispatch a check for your 2020 and/or 2021 FFCRA tax credit directly to the address linked with your IRSPlus account. It's like getting a special delivery just for you. But, keep in mind, if you've got any outstanding tax dues, the IRS will play the balancing act - using your refund to square off these liabilities first.

Eagerly awaiting your refund? Let's break down the timeline: Once you've filed for your FFCRA credit, the IRS typically takes up to three weeks to give you a nod of acceptance. Think of it as the IRS giving your application a thumbs up. But the real countdown begins after this acceptance – it can take 16 to 20 weeks for your refund to make its grand entrance, via check.

If you find yourself with questions or in need of assistance as you navigate through the process, don't worry, we've got your back! Our dedicated customer service team is like your personal support squad, ready to jump in and make sure your experience is as smooth and stress-free as possible.

No matter where you are in the process, if you hit a snag or just need some clarification, we're only a message or a call away. Our team is always on standby, eager to assist you with any inquiries or concerns. Reach out to us through our designated channels, and we'll be right there to guide you, ensuring you have all the information and support you need. We're here to make your journey through this process as straightforward and hassle-free as we can. Your peace of mind is our top priority!

No need to worry about overwhelming paperwork. Our process is straightforward and secure:

Effortless Agreement Signing: You'll receive a secure email to sign our “Client Agreement” electronically. Quick and easy!

Minimal Documentation: Just upload your tax returns for 2019, 2020, and 2021, along with your driver’s license and a secondary photo ID for compliance.

We Handle the Details: Once your documents are uploaded, our team takes over, managing everything from amendments to maximizing your entitlements.

Already Filed Your Taxes? If you've filed your 2020 and 2021 returns but need amendments for additional credits, we're here to help with that too.

That's it! We aim to make this process as seamless and efficient as possible for you.

Clock's ticking, but there's still time! Here's the lowdown on those crucial FFCRA tax credit deadlines:

2020 Returns: The magic date for your 2020 tax return is April 15, 2024. It's your key opportunity to claim those FFCRA credits for 2020.

2021 Returns: For your 2021 tax return, circle April 15, 2025, in your calendar. That's your deadline to get those credits for 2021.

And here's a handy rule of thumb: You've got either three years from the original due date of your return or two years from when you paid the tax (whichever comes later) to make any amendments for claiming or adjusting your FFCRA credits. So, if you're looking to tweak your 2020 or 2021 returns for some extra credit, keep these dates in mind.

FFCRA (Families First Coronavirus Response Act) isn't a loan and not quite a grant either. Think of it as a tax credit – a way to get back some of the taxes you've already paid. Here’s how it stands out:

Refund, Not a Loan: Since it's a tax credit, it functions as a refund of taxes you've already contributed, not as a borrowed amount you need to repay.

Mimics Paid Leave Expenses: The structure of FFCRA credits mirrors the kind of support that mandatory paid leave provides to employees. It’s geared to cover expenses similar to those incurred during paid leave.

Worry not about your 2023 tax filings when claiming FFCRA tax credits – they're like two ships passing in the night, not affecting each other. Here's the lowdown:

Separate Lanes: Filing for FFCRA credits is a journey back in time, revisiting your 2020 and 2021 tax filings. It's all about making tweaks to those years, not the upcoming 2023 tax season.

Expert Navigation: Our CPA crew is like your time-travel team, diving into your past filings (2020 and 2021) to skillfully amend them for FFCRA credits. They ensure everything's shipshape without causing ripples in your 2023 tax voyage.

Smooth Sailing for 2023: Your 2023 tax filing remains unaffected, cruising along its usual course. So, you can breathe easy and focus on the here and now, knowing your past and future tax journeys are well taken care of.

You're considered self-employed by the IRS if:

You operate as a sole proprietor or independent contractor. You're a member of a partnership conducting a trade or business. You run any form of business yourself, including part-time or gig work.

Note: Self-employment income on Form 1040-SE is key for SETC eligibility. General partners' income counts from all business income, while limited partners' income is only from guaranteed service payments. For amendments, you can use 2019 or 2020 income for 2020, and 2020 or 2021 income for 2021 filings.

To be eligible for FFCRA tax credits, here's what you need:

Your Work Profile: You should be self-employed - think sole proprietors, independent business owners, 1099 contractors, freelancers, gig workers, or single-member LLCs.

Tax Filing Details: You must have filed a Schedule SE with your IRS Tax Form 1040 for either 2020 or 2021, showing positive net income and having paid self-employment tax on your earnings.

COVID-Related Work Absence: The key reason for missing work should be COVID-19 related, like being under a government-imposed quarantine or isolation order, or following a doctor's recommendation to self-quarantine.

If you tick these boxes, you're likely in the zone for FFCRA tax credits. Need more info or have other questions? Just let me know!

To qualify for FFCRA tax credits, it's essential that your work as a self-employed individual was interrupted due to specific COVID-related reasons. These include:

Quarantine Orders: Being unable to work because of quarantine or isolation orders imposed by a government agency.

Self-Quarantine Advice: Following a recommendation by a healthcare provider to self-quarantine.

Symptoms and Diagnosis: Experiencing COVID-19 symptoms and seeking a medical diagnosis or awaiting test results.

Vaccination and Side Effects: Missing work due to getting vaccinated against COVID-19 or dealing with its side effects.

Virtual school and School Closure Challenges: Caring for children during school or daycare closures caused by the pandemic.

Caring for Affected Others: Providing care for a family member who is dealing with COVID-19 related issues.

These criteria cover a broad spectrum of COVID-19 impacts, from health concerns to caregiving responsibilities, ensuring comprehensive support through the FFCRA.

If you have more questions or specific aspects you'd like further information on, feel free to ask!

Absolutely, there are a few key limitations to the Self-Employed Tax Credit (SETC) that are worth keeping in mind:

Not a Full Payout with Other Benefits: If you've already received wages from an employer for sick or family leave in 2020 or 2021, don't expect to hit the SETC jackpot. Your SETC amount gets trimmed down by the FFCRA wages you pocketed.

Unemployment Benefits Affect the Equation: Also, if you received unemployment benefits during these years, your SETC calculation needs to sidestep these days. It's all about ensuring you're not double-dipping from the benefit pool.

Residency Matters: And remember, SETC isn't just for anyone. You need to be a U.S. citizen, permanent resident, or a qualifying resident alien to get in on this.

Income Limits in Play: There's also an income ceiling to consider. Earning beyond a certain threshold might nudge you out of the SETC eligibility zone.

Geographical Variations: Different countries have their own spin on SETC rules. It's wise to consult a tax professional or dig into your country's tax guidelines to see where you stand.

So, while SETC offers a valuable financial cushion, it's not a one-size-fits-all deal. Knowing these limitations helps you realistically assess what you can expect from this credit.

The FFCRA tax credits cover specific periods for those unable to perform self-employment work due to COVID-19. Here's a detailed breakdown:

This detailed timeline gives a clear view of the eligible dates and the amount of time you could potentially claim under the FFCRA tax credits.

Certainly! If your 2020 or 2021 taxes are still pending, you're not out of the race for SETC benefits. Our team of Accountants are well-equipped to prepare your original tax returns with the inclusion of SETC. But remember, it's important to be aware of the refund statute limitations discussed earlier.

This ensures that you remain within the legal timeframe for claiming your tax credits. Our professionals are here to guide you through this process, making sure you meet all necessary requirements for a successful SETC claim.

Yes, W2 employees can claim FFCRA tax credits, particularly if they have self-employment income in addition to their W2 salary from 2020 and/or 2021. However, it's important to understand the nuances:

Qualifying for the SETC (State Earned Tax Credit) remains possible even if you received unemployment benefits during the pandemic years of 2020 and 2021. However, it's important to note a critical distinction: the days for which you received unemployment benefits cannot be claimed as days of inability to work due to COVID-19 related issues.

This distinction is crucial for accurately determining your eligibility for the SETC tax credit. To navigate this complex scenario and ensure compliance with state tax laws, consulting a tax professional is highly advisable for tailored advice.

Self-employed individuals in 2020 or 2021 have the flexibility to elect either their 2019 or 2021 income for SETC purposes if self-employed in 2020, and either 2020 or 2021 income if self-employed in 2021. However, remember, if you receive employee paid leave benefits, it affects the FFCRA tax credit you can claim as a self-employed individual. It's crucial not to claim overlapping benefits for the same period under the FFCRA, but you may be eligible for additional credits based on self-employment income if employee benefits don't fully cover your situation.

Certainly! To claim SETC credits, you'll need to reassess your 2020 or 2021 tax returns. This involves a bit of homework on your eligibility and some number crunching. Of course having a good understanding of the tax credits tax code will help you solidify your eligibility and maximize your refund. We’ve invested in all the supporting government orders by State, city and county so can support your claim properly.